9

Cosmetic Industry in Figures

“Clearly, the report covers a wide range of markets and the

story has changed within some of them, if we take the three

biggest, fragrance, colour cosmetics and skincare we see

colour cosmetics bucking the trend. An increase of 1.6% in

packs is encouraging but 7% value growth highlights that

shoppers (in this case females) are prepared to spend to make

themselves look good, feel better and have the right products

to choose. Lipsticks have done very well as have all the other

sectors except nail varnish (which had a good 2014).

“Fragrance has had another tough year as we see a 3% fall

in sales, there are less buyers but it is Christmas gifting that

is worrying as it has become less popular to include perfumes

and aftershaves as part of the ritual Christmas gifting

behaviour. Black Friday also causes a disruption as some

purchasing is made earlier than normal.

“The varied skincare market has seen mixed fortunes.

Prestige value has fallen but mass facial skincare and body

care has fared somewhat better as shoppers loosen their

spending a little, this has not translated to men’s skincare

though, the proliferation of beards hasn’t helped this sector!

“Mass market sectors like haircare and deodorants have been

victims of the price war i.e. grocers have started to match

discounter pricing so the public get lower prices but it hasn’t

encouraged greater quantities to be bought. In fact, volume

is down further than value (1.6% value v 3.1% yr/yr decline

in units) with shampoo and conditioners suffering, however,

fashionable styling products have performed much better.

“Footcare is another oasis of market growth as more products

are aimed at this area that may have been neglected in the

past. Liquid soap has managed growth at the expense of

bar soap whilst shower products see improved unit sales but

discounting has led to a value fall of nearly 1%.

“2016 looks as if we will see a similar pattern as 2015

as discounters continue to improve market share.

Multiple grocers are losing share (losing 1.1 percentage

share points from 2014 now at 28.9%) not just to the food

discounters (Aldi/Lidl) but also to the bargain stores such

as Home Bargains and Poundland. Discounters now have

6.5% share from 6.1% share in 2014.

“Department stores and perfumery outlets (where beauty

is the main focus) have maintained a 14.9% share whilst

duty free (shops in international travel hubs) have experienced

leaner times. Interestingly for total cosmetics, the High Street

is in revival and chemist and drugstore sales are on the up

with this channel taking 35.7% value share (from 35.5% in

2014) so the story is not entirely around price and discounting.

“2016 does not look to be a boom year but economic

indicators should help with the more prestige markets and it

remains key that manufacturers continue to cater for needs

of the consumer in all the categories – not just on price but

on quality and availability. Internet shopping, (internet only

e-tailers) has seen flat sales year on year but in some markets,

fragrance for example, total internet (all sites) sales exceed

21% of all sales.”

“ The UK cosmetic and personal care market followed a similar pattern in 2015 to that of 2014 in that we

see an overall decline in value of the market year on year (yr/yr) of 0.2% (0.1% 2014 v 2013) and a fall

in actual packs purchased of 0.3% yr/yr (0.5% 2014 v 2013). Essentially, shoppers have become used

to searching for bargains and price has become the key driver as opposed to multi-buys, for example in

grocers and chemists that drove volumes in the past.”

Tim Nancholas

Strategic Insight Director – Home, Health & Beauty, Kantar Worldpanel, March 2016

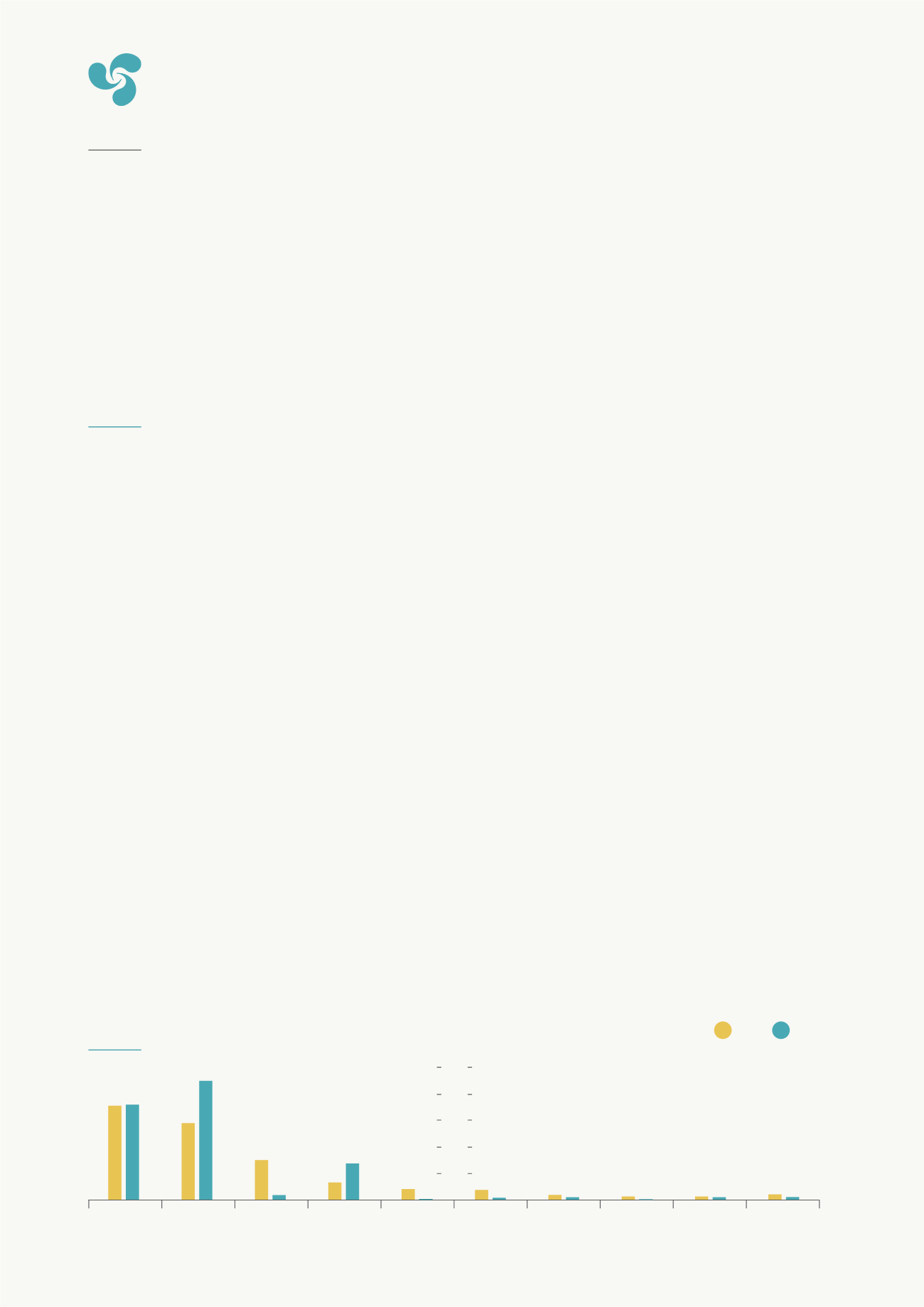

Chemist &

Drugstores

Grocery

Perfume &

Department

Stores

Discounters

Cosmetic

Specialists

Pure Internet

Direct

Clothing &

Specialists

Duty Free

All others

Value

Units

CTPA Categories Channel share % Value / Units

10%

20%

30%

40%

35.7 35.8

13.7

45

28.9

14.9

1.7

6.5

4

2 1.01

0.11

0.11

3.7

0.7

0.9 1.8

1.2

0.9 1.2

50%

28